[vc_row][vc_column][vc_column_text]

A word we use quite often when talking about food and beverage brands is categories. And it turns out, what “category” means in the context of a grocery store is more difficult to define than you might think.

We advocate beginning everything in your business with meeting an unmet consumer need. So, categories could be defined as groups of products that meet a similar consumer need or that can substitute for each other. This allows something like snacks, as a category, to cover many different types of products and have a plethora of sub-categories (salty snacks, sweet snacks, etc.). What makes sense to consumers might make less sense to you, and you don’t have that much time to communicate with consumers in the grocery store.

There are practical challenges to categorization as food and beverage brands seek to grow their businesses. Different categories have different buyers at grocery stores, and it can be a struggle to develop relationships with buyers only to have to start over because you positioned yourself in the wrong category. And, certain categories are growing more than others or are more crowded than others, limiting potential top-line sales growth. This should be considered before launching a business or ramping up production of products.

The reality is, for food and beverage brands, the dynamics of the category they are in can mean life or death. Retailers might define your product by in-store location only, and this placement in-store might conflict with your ideal positioning or the story you are telling to your target consumer. This dynamic is especially true with companies that have products that have a legitimate claim to multiple categories. If you are positioning your product as a snack but it looks like a bar, a placement in the bar section might mean less sales and eventually losing that store.

Food and beverage businesses should define what category they are in and make sure their salespeople and brokers develop relationships with the right category buyers. That definition and clarity is needed to be properly placed in stores and hopefully get off the shelf.

And now, our roundup of the best food and beverage finance news, events and resources from around the web…

Business Model Insights

- Costco’s Business Model Is Smarter Than You Think (Investopedia) – “Costco’s business model is called a subscription business model. Customers who want to shop at the store must buy a membership with the promise of lower prices to make up for the initial upfront cost. While other stores may have occasionally lower prices on their loss leaders, Costco has permanently capped its margins to ensure that members can justify paying for a membership. Costco employees also earn a decent wage, saving money by making them more productive and less likely to quit. Costco has a policy of carrying a lower number of products than traditional grocery stores. Having fewer products to order, track and display means cost savings for Costco. And, by having a limited retail space, suppliers must bid for Costco shelf space to get their products sold.”

- Finding opportunity at the intersection of food production and distribution (Food Dive)

- Making a killer impression starts with standout founders (New Hope Media)

Raising Capital

- One investor’s must-haves and red flags for natural brands seeking funding (New Hope Media) – “There are a few really important valuation drivers for younger CPG companies in the natural category. First, make sure you are not a ‘me too’ company. Be differentiated and positioned for growth in an accelerating category. Another important thing? Having broad and deep sales in a category or geographic area. It’s a challenge for investors to get their arms around where the real opportunity is if you’ve only got sales with one or two or three customers. Or, there’s one customer that represents 50 percent of your sales, which doesn’t give the investor any sort of leeway if that customer goes away.”

- How Investors Can (and Can’t) Create Social Value (Stanford Social Innovation Review)

- Get out there and get fearless about funding [infographic] (New Hope Media)

CPG/National Brands

CPG/National Brands

- Retailers find fresh solutions for their most challenging—and critical—categories (New Hope Media) – “Stroll down the aisles of Natural Products Expo West or Natural Products Expo East and you’ll discover innovations in packaged foods galore. What you won’t see at many trade shows, however, is much creativity surrounding key grocery store products such as perishable grab-and-go items and fresh produce that actually capture a significant portion of natural retail sales. In response, retailers are prioritizing categories such as produce, dairy and grab-and-go to offer a point of differentiation. That difference can be described as “fresh.” Produce, dairy and grab-and-go offer shoppers something that online sales can’t: the opportunity to examine, smell, feel and ultimately buy specific fruits, vegetables and other ready-to-consume items themselves.”

- 10 Forces That Have Caused the Packaged Food Startup Explosion (Entrepreneur)

- Grocery, disrupted: 5 minutes with Future Market’s Mike Lee (New Hope Media)

Market Trends

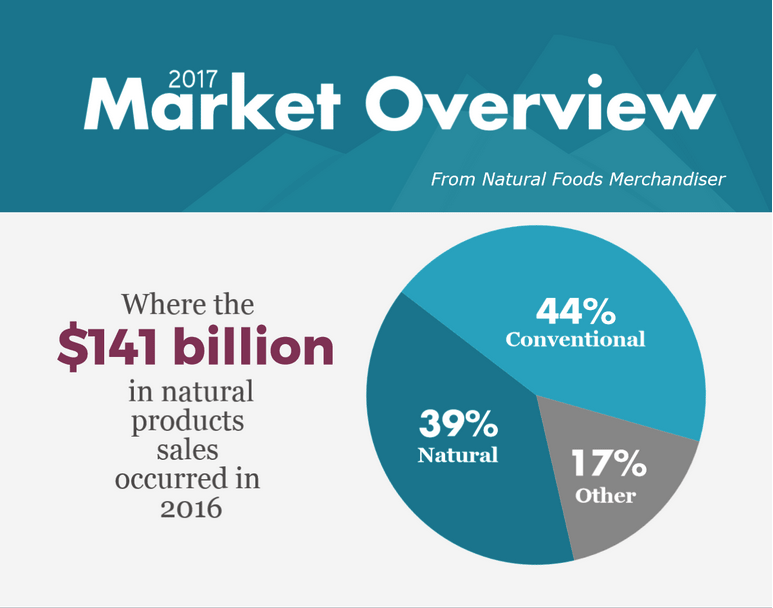

- Market Overview: Sizing up 2016 organic and natural products retail sales (New Hope Media) – “With its childhood innocence in the distant past and the erratic growth spurts of adolescence now behind it, the $141 billion natural products industry moved firmly into adulthood in 2016, maturing to a modest 7.4 percent growth rate across all channels, with independents and natural chains slowing to a 4.3 percent year-over-year change. Competition remained heated, with conventional stores now selling a whopping 44 percent of all natural products, compared to 39 percent sold in natural products stores.”

- Snackification Takes Hold (Convenience Store News)

- Special Report: Gluten-free enters the mainstream (Food Business News)

Farming and Ag Tech

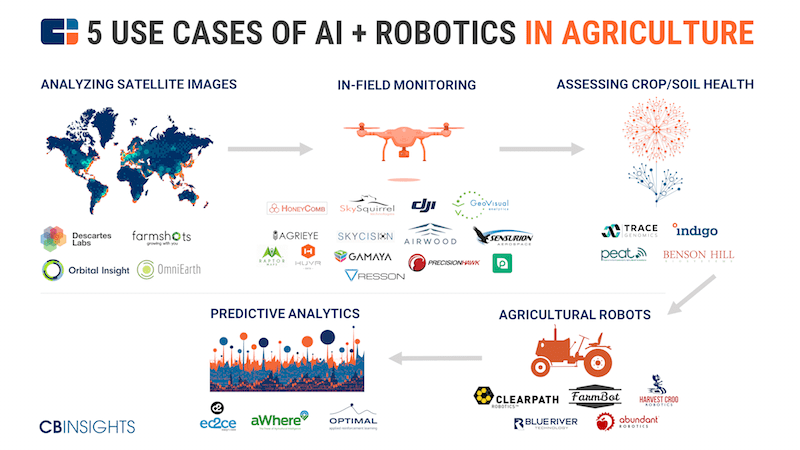

- AI, Robotics, And The Future Of Precision Agriculture (CB Insights) – “Agricultural tech startups have raised over $800M in the last 5 years. Deals to startups using robotics and machine learning to solve problems in agriculture started gaining momentum in 2014, in line with the rising interest in artificial intelligence across multiple industries like healthcare, finance, and commerce.”

- Do-It-Yourself Approaches Are Common In Wisconsin Aquaculture (Wiscontext)

- Proactive Management, Cow Comfort Keys to Organic Farming Success (MidWestern BioAg)

Deals/M&A

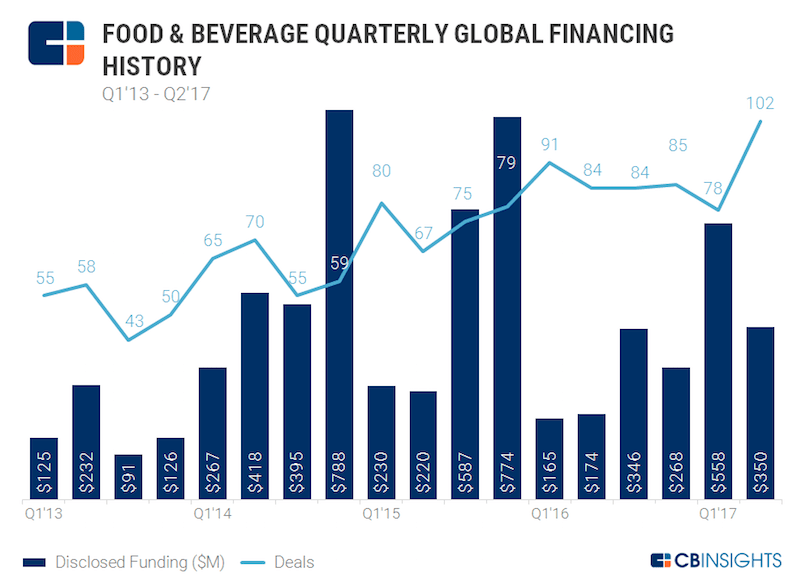

- Food & Beverage Deals Hit New High (CB Insights) – “Deals to private food and beverage companies hit an all-time high of 102 in Q2’17, growing 31% from the previous quarter. If this investment pace continues throughout the second half of the year, 2017 may see new records in both deal count and investment dollars to the food and beverage industry. Recently launched corporate venture funds led by top food corporates (including Campbell Soup, General Mills, and Kellog’s) contributed to the quarter’s growth as they continued to ramp up their activity, while there was also notable growth in beverages, which captured four of the quarter’s five largest deals.”

- Big food companies are trying to reverse the curse of the center aisle (CNBC)

- The Amazon–Whole Foods Deal Means Every Other Retailer’s Three-Year Plan Is Obsolete (Harvard Business Review)

Industry Events

- FabCap Accelerator Applications – Free, Applications due 8/16

- Natural Products Expo East (New Hope Network) – $, 9/13 – 9/16 in Baltimore, MD

[/vc_column_text][/vc_column][/vc_row]